The anti-fog additives market, essential for applications in food packaging, agriculture, and automotive sectors, is projected to grow significantly in the coming years. Anti-fog additives prevent condensation on plastic surfaces, maintaining visibility and improving product aesthetics and functionality. As the market expands, it faces both promising opportunities and distinct challenges.

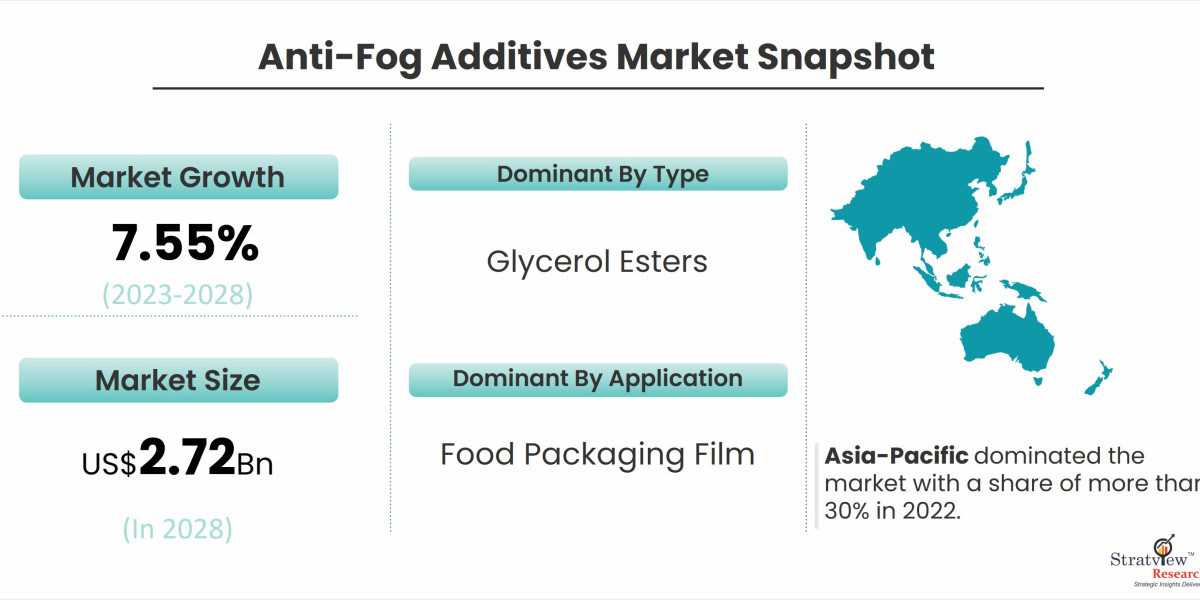

According to Stratview Research, the anti-fog additives market was estimated at USD 1.75 billion in 2022 and is likely to grow at a CAGR of 7.55% during 2023-2028 to reach USD 2.72 billion in 2028.

Key Opportunities in the Anti-Fog Additives Market

- Increased Demand in Food Packaging: The food packaging industry remains the largest consumer of anti-fog additives. Rising global demand for fresh and visually appealing packaged foods, especially in urban centers, fuels this need. With more consumers seeking ready-to-eat and packaged food, manufacturers are investing in advanced anti-fog solutions to improve shelf appeal and prevent spoilage. This trend is particularly strong in North America, Europe, and Asia-Pacific, where strict food safety standards and consumer expectations drive continuous innovation in packaging.

- Growth in Greenhouse Agriculture: The agricultural sector, particularly greenhouse farming, relies on anti-fog additives in plastic films to enhance light transmission, which supports healthy plant growth. As demand for high-yield crop production increases, especially in regions with challenging climates, the need for anti-fog solutions in agriculture will grow. Regions such as Europe, where greenhouse farming is prevalent, are key markets for these additives, and expanding markets in Asia-Pacific offer additional opportunities.

- Sustainability and Biodegradable Solutions: Increasing environmental concerns are pushing manufacturers to develop eco-friendly, biodegradable anti-fog additives. Many countries, especially in Europe, have imposed stricter regulations on single-use plastics, driving innovation in sustainable additives. This trend creates opportunities for companies to develop green alternatives that cater to both regulatory demands and consumer preferences for environmentally conscious products.

Key Challenges in the Anti-Fog Additives Market

- Regulatory Compliance and Environmental Standards: The push for sustainability also presents a challenge. Regulatory agencies worldwide are setting stringent environmental standards for plastic packaging and agricultural films. Adapting to these evolving standards requires manufacturers to invest in R&D for biodegradable and less toxic alternatives, which can increase production costs and limit options.

- Fluctuations in Raw Material Prices: Anti-fog additives often use petroleum-based materials, making them susceptible to fluctuations in oil prices. These price changes can impact production costs and profit margins for manufacturers. In response, companies are looking for renewable raw materials, but developing these alternatives can be costly and time-consuming.

- Technological Barriers: Developing effective anti-fog additives that maintain clarity without compromising other properties like durability remains challenging. Achieving optimal performance, especially for biodegradable solutions, requires advanced technology and formulation expertise, which can limit market entry for smaller players.

Conclusion

The future of the anti-fog additives market is marked by exciting growth opportunities in food packaging and agriculture, along with a strong shift toward sustainable solutions. However, the industry must navigate challenges like regulatory pressures, volatile raw material costs, and technical hurdles to capitalize on these opportunities. Companies that prioritize innovation, focus on sustainable practices, and adapt to evolving market needs are well-positioned to succeed in this dynamic market.